The first trap is lifestyle inflation. Each time you get a raise, your spending increases as well. Your quality of life improves, but your savings rate stays the same. You maintain the same savings ratio at a higher level of consumption. The way out is simple. Each time you get a raise, put a portion of the increase directly into savings.

The second trap is focusing on monthly payments instead of the total price. Installment payments make large expenses seem cheaper. A small monthly payment feels easier than one large payment. But the total price is the same, or even higher due to interest. The way out is to convert every installment plan to the total price and ask yourself whether you would pay that amount in one lump sum.

The third trap is the sunk cost fallacy. You have already spent a lot of money on something, so you keep going even when you know it is not wise. Past spending should not influence future decisions. The only question is: From this point forward, which choice is better? Ignore what you have already spent and decide based only on the future.

The fourth trap is social comparison. You see that your neighbor bought a new car, your colleague went on a faraway vacation, and your friend hired an expensive private tutor for their child. You feel left behind, so you start spending more too. But you are seeing the surface of others’ lives, not their full financial picture. Stop comparing yourself to neighbors. Compare yourself only to your past self.

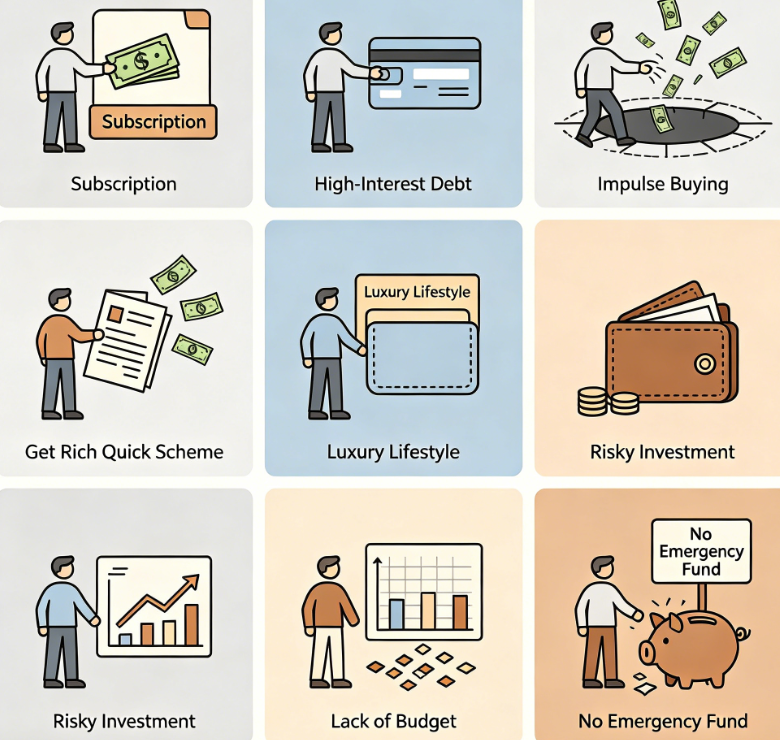

The fifth trap is the blind spot for small expenses. A few dollars for coffee, a few dollars for delivery fees, a few dollars for app subscriptions. These small expenses seem insignificant on their own, but they add up to a significant amount each month. The way out is to track every small expense for a set period and then decide which ones to cut.

The sixth trap is the minimum payment trap. Your credit card statement shows a minimum payment amount, and you think paying that is enough. But the remaining balance continues to accrue interest. The minimum payment is designed to keep you in debt for a long time. The way out is to never pay only the minimum. If you cannot pay the full amount, at least pay a fixed higher amount.

The seventh trap is saving last. Each month, you pay all your bills, and then if anything is left over, you save it. Usually, nothing is left. The way out is to reverse the order. On payday, transfer savings first, and then use the remaining money to pay bills and living expenses.

Financial freedom is not an unreachable goal. It is the accumulation of many correct choices. Identify which traps you have fallen into, and then start changing them today.