The first option is a Health Savings Account. If you have a high-deductible health insurance plan, a Health Savings Account is your next best choice. This account offers triple tax advantages. Contributions are tax-free. Growth is tax-free. Withdrawals for medical expenses are tax-free. No other account offers this triple tax benefit.

The second option is a Roth Individual Retirement Account. A Roth IRA is funded with after-tax money, but withdrawals in retirement are completely tax-free. If your income is below a certain level, you can contribute directly. If your income is too high, you may consider the backdoor Roth strategy, converting from a Traditional IRA.

The third option is a Spousal IRA. If you are married, you can open and fund an IRA for your spouse based on your income, even if your spouse has no earned income. This effectively doubles your family’s tax-advantaged savings space.

The fourth option is a 529 education savings plan. If you have children or plan to have children in the future, a 529 plan is a tax-advantaged education savings tool. Many states offer additional tax deductions. Even without children, you can open a 529 plan for yourself for future continuing education.

The fifth option is a taxable brokerage account. After you have exhausted all tax-advantaged accounts, the next dollar goes into a taxable account. While there are no tax advantages here, there are also no contribution limits or withdrawal restrictions. You can access your money at any time, and your investment choices are the broadest.

The sixth option is the mega backdoor Roth. This strategy only works if your employer retirement plan allows after-tax contributions and in-plan Roth conversions. If allowed, you can move significantly more money into a Roth account than the normal limits would permit.

The seventh option is paying down high-interest debt. Before investing, make sure you have paid off all high-interest debt. Credit card interest is typically far higher than any investment return. Pay off debt first, then invest.

The eighth option is building or replenishing your emergency savings. Emergency savings are the foundation of your financial security. Make sure you have enough cash for unexpected expenses. Do not put all your extra money into long-term investments.

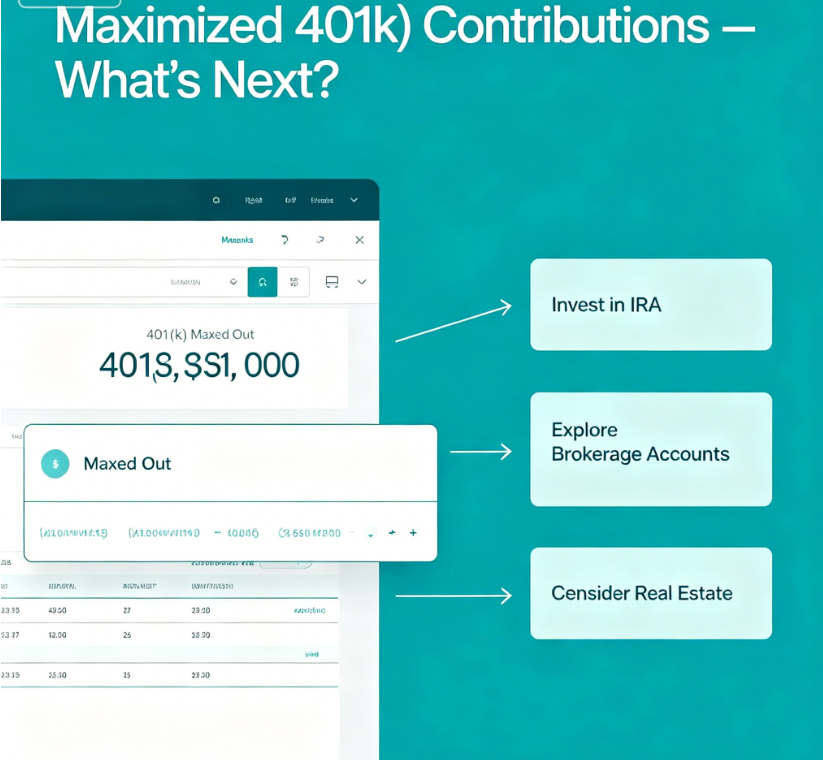

You have already taken the most important step: maximizing your 401(k). The next choice depends on your personal situation, your goals, and the tools available to you. Evaluate your options and make the decision that best fits you.