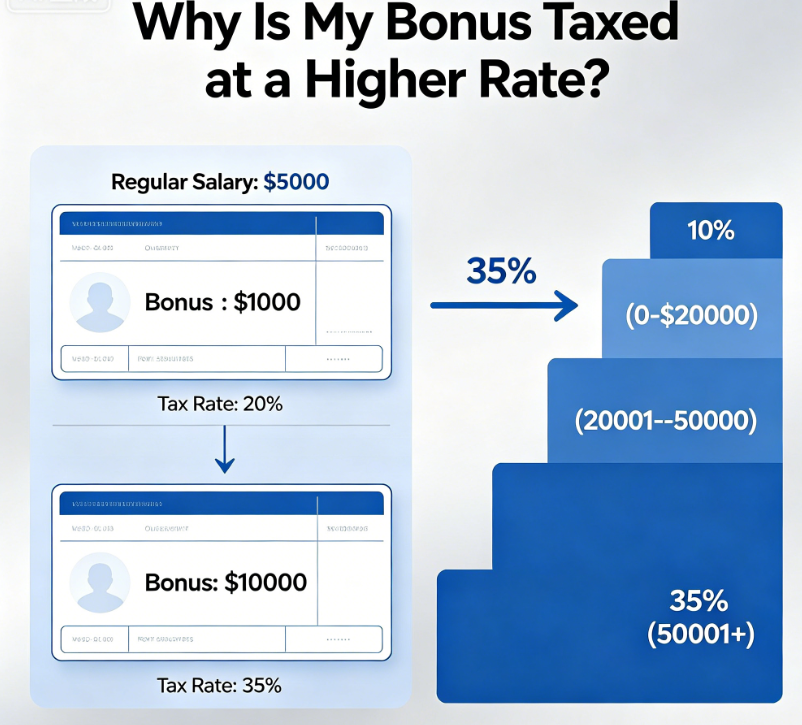

When a company pays a bonus, it must withhold taxes according to tax laws. Withholding is not your final tax bill. It is an estimate. Most companies use the percentage method for separately paid bonuses, withholding a flat federal rate. This flat rate is the legally required standard method. It is not adjusted for your personal situation. If your marginal tax rate is lower than this flat rate, you will feel that your bonus was over-withheld. If your marginal tax rate is higher than this flat rate, you will feel that your bonus was under-withheld.

If your bonus is paid together with your regular salary, the situation is more complex. The payroll system annualizes the total income for that month and withholds taxes based on that annualized income. This can result in a withholding rate that appears very high, because the system assumes you receive this high income every month. For example, if you receive your regular monthly salary plus a significant bonus in one month, the system assumes that you earn this high amount every month of the year. It then applies the highest tax bracket to your withholding. This is a conservative estimation method. It prefers to over-withhold rather than under-withhold, because over-withholding results in a government refund while under-withholding requires you to pay additional tax.

In addition to federal tax, your bonus is also subject to Social Security tax and Medicare tax. These taxes have fixed rates that do not change with income level. No matter how high your income, these tax rates remain the same. State tax is also withheld from your bonus. The specific rate depends on your state. Some states have special rules for bonus withholding, while others treat bonuses as ordinary income. All of these together explain why your take-home bonus appears much smaller than expected. You are not seeing a single tax. You are seeing the sum of multiple taxes.

The key is understanding the difference between withholding and actual tax liability. Withholding is what is taken from each paycheck. It is an estimate. Actual tax liability is the total tax you calculate when filing your tax return next year. It depends on your total annual income. Withholding is an estimate. Actual tax liability is the precise amount. If your total withholding exceeds your actual tax liability, you receive a refund. If your withholding falls short, you owe additional tax. Most people prefer to receive a refund rather than owe money at tax time. Therefore, the withholding system is designed to be conservative, tending to over-withhold rather than under-withhold.

For bonuses, the withholding rate may appear high, but that does not mean you are being overtaxed. When you file your tax return next year, your bonus and your regular salary are combined and taxed at your actual marginal tax rate. Your marginal tax rate is the amount of additional tax you pay for each additional dollar you earn. If your total income is high, your marginal tax rate will also be high. If your marginal tax rate is lower than the bonus withholding rate, you will receive a refund. If your marginal tax rate is higher than the bonus withholding rate, you will owe additional tax.

If you regularly receive large bonuses and find yourself owing money at tax time each year, you can adjust your withholding settings. File a new withholding form requesting an additional amount to be withheld from each paycheck. This spreads your tax obligation throughout the year, avoiding a large lump sum payment next April. This is a common method used by high-income earners. They prefer to have a little more withheld each month rather than face an unexpected large tax bill at filing time.

Another strategy is to put part of your bonus into a tax-deferred retirement account. If you have not yet reached your annual retirement account contribution limit, you can ask your company to deposit a portion of your bonus directly into that account. This money is not taxed now, while also saving for your future. This is a win-win strategy. You lower your taxable income for the current year while increasing your retirement savings. However, be aware that money in tax-deferred retirement accounts is still taxed when withdrawn, unless you are using a Roth account.

Do not let bonus withholding discourage you from working hard or accepting a bonus. Your bonus is your earned income. The taxes withheld are just paid in advance. Everything is settled when you file your tax return. You should focus not on the withholding rate, but on your actual annual income and your actual annual tax liability. Withholding is just a cash flow management issue, not a true tax burden issue. If you were over-withheld, you get a refund. If you were under-withheld, you pay the difference. Either way, your actual tax liability is determined by your total annual income, not by the withholding from any single month.