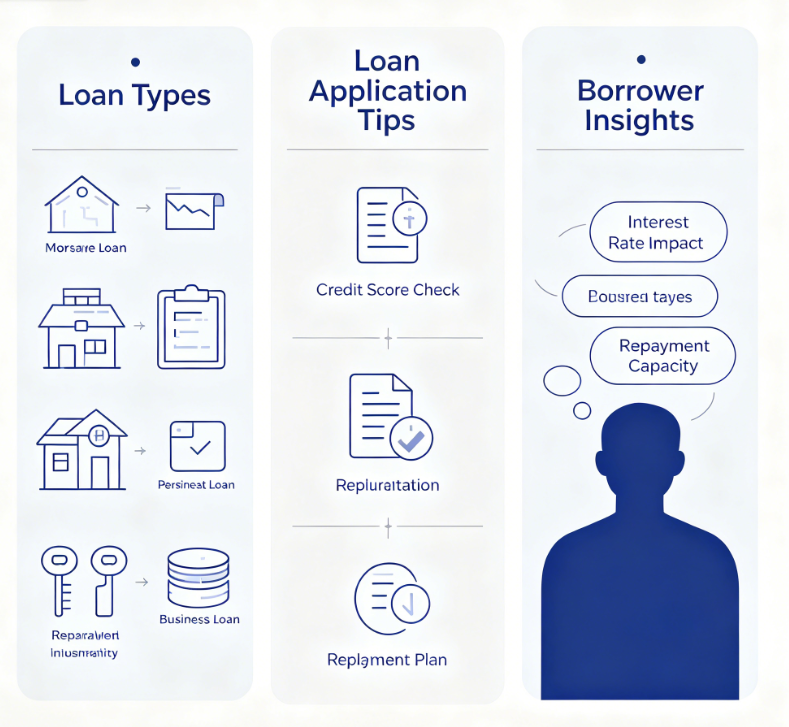

By purpose, there are many types of loans. Personal loans are for various purposes like medical bills, weddings, or debt consolidation. You do not need to state the purpose, and the interest rate depends on your credit. Student loans are for education costs. Government student loans have lower interest rates and flexible repayment. Private student loans have higher rates. Auto loans are for buying a car. The car serves as collateral. Mortgages are for buying a home. The home serves as collateral. Mortgages have long terms and relatively low rates. For most people, this is the largest loan they will ever take. Business loans are for business purposes. The bank looks at the business’s profitability and your personal credit.

By collateral, there are secured and unsecured loans. Secured loans require collateral such as a house, car, or savings deposit. If you do not repay, the lender can take the collateral. Because the risk is lower, the interest rate is lower. Unsecured loans do not require collateral. The lender trusts you to repay. Because the risk is higher, the interest rate is higher. Credit cards and personal loans are typically unsecured. Secured loans provide a safety net for lenders, allowing borrowers to get better terms.

The core concepts of loans include principal, interest, term, annual percentage rate, and fees. Principal is the money you borrowed, not including interest. Interest is the price you pay for borrowing. Term is how long you have to repay. Short-term loans last months. Mortgages can last up to thirty years. APR is the true annual cost of the loan, including interest and certain fees. When comparing loans, compare APR, not just the interest rate. Fees include application fees, appraisal fees, and prepayment penalties. These fees increase your actual cost. A loan that looks cheap because of a low interest rate may not be so cheap when you add up all the fees.

Your credit score is a number lenders use to judge your reliability. A higher score means you are more likely to pay on time. Benefits of a high credit score are lower interest rates, higher borrowing limits, and faster approval. A low credit score can lead to rejection or approval at very high interest rates. Your credit score is based on whether you pay on time, how much of your available credit you use, how long you have had credit, whether you have different types of credit, and how many new credit applications you have made recently. Even with a lower score, you may still get a loan. It will just cost more. Improving your credit score takes time, but each on-time payment helps.

Before taking a loan, ask yourself several questions. Do you really need this loan? Some expenses can wait. Some can be paid from savings. A loan should be the last choice, not the first. Can you afford the monthly payments? Not just this month’s payment, but every month’s payment until the loan is paid off. What is the total cost? Add up all the interest and all the fees. Is there a cheaper option? Borrow from family, use savings, or wait instead of borrowing. What happens if you cannot repay? What are the consequences? These questions help you distinguish necessary loans from unnecessary ones.

Borrowing responsibly means borrowing only what you need, understanding what you sign, setting up automatic payments to avoid forgetting, and checking for prepayment penalties if you plan to pay early. Do not treat a loan as income. A loan is debt, not income. Do not borrow to maintain a lifestyle beyond your means. This is the most common mistake in borrowing. People borrow more than they need to support a standard of living they cannot afford, eventually falling into debt trouble.

A loan is a tool. A good loan has a reasonable interest rate, terms you understand, payments you can afford, and is used for something you need. A bad loan has a high interest rate, terms you do not understand, payments that strain you, and is used for something you do not need. Before you sign, take time to understand what you are signing. Ask questions. Ask someone to explain terms you do not understand. A loan contract is a legal document. You have the right to understand it fully before signing.

Finally, remember that a loan is not free money. It is an advance on your future income. Every dollar you borrow must be repaid with future labor. Before you enjoy the immediate gratification of a loan, consider whether your future self will be willing to pay the price. Smart borrowers respect money, and they also respect their future selves.