Distinguishing the time horizon of your goals is the first step. The shorter your time horizon, the lower your tolerance for risk. Money you need within two years should not be invested in the stock market, because the market could be at a low point exactly when you need the money. You cannot predict market timing, so you should keep short-term money in safe places. The longer your time horizon, the higher your risk tolerance. If retirement is decades away, you can withstand market fluctuations because you have plenty of time to wait for recovery. Historical data shows that investors who hold quality assets for the long term almost always achieve positive returns.

Setting specific numbers for each goal is the second step. Vague goals cannot be executed. “I want to save money” is not an actionable goal. “I want to save a specific amount by a specific date” is a clear goal. Clear goals allow you to work backward. You can calculate how long you have and how much you need to save each month. If your calculation shows that the required monthly savings exceed your capacity, you have several choices. You can extend your target date, which lowers the monthly savings requirement. You can reduce your target amount, accepting a smaller but more realistic outcome. You can increase your income through a side job or overtime. Clear numbers force you to face reality rather than clinging to false hope.

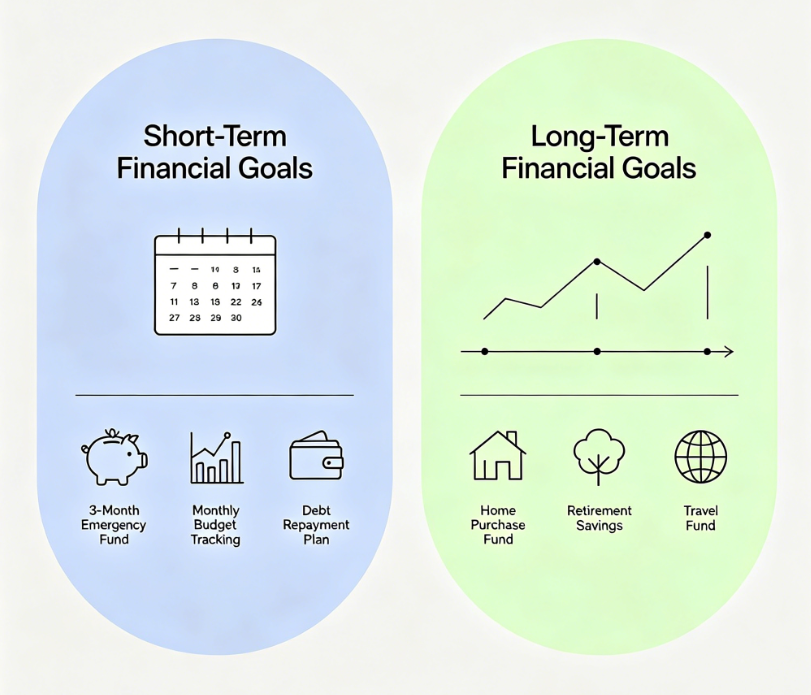

Choosing the right tools for each goal is the third step. Short-term goals belong in safe, liquid places such as high-yield savings accounts or money market funds. These tools will not lose principal, and you can access your money at any time. Medium-term goals may be suited for balanced investments that hold both stocks and bonds. This combination provides some growth potential while reducing volatility. Long-term goals can be allocated more heavily to stocks, because stocks have historically offered the highest returns over long periods. Although stocks are highly volatile in the short term, the long-term trend is upward.

Setting up multiple separate accounts or sub-accounts is the fourth step. Mixing money for different goals in the same account creates confusion. You might think you have saved a lot, but that money may already be allocated to another goal. You can open a separate sub-account for each goal or track them separately in your budget. This allows you to see the progress of each goal clearly. When you look at one goal, you are not distracted by the balances of other goals.

Automation is the fifth and most critical step. Willpower runs out, but automation does not. Set up automatic transfers for a fixed amount on a fixed day each month. Money will flow automatically from your checking account to your various goal accounts. You do not need to make a decision each time, and you are less likely to dip into goal funds on impulse. Automation turns saving from a task that requires willpower into a habit that requires no thought. This is one of the key differences between the wealthiest investors and ordinary investors.

Regular progress reviews are the sixth step. Review your progress at least once a year to see if you are on track. Life does not stay the same. You will change jobs, move, get married, and have children. These changes affect your financial goals and your capacity. An annual review gives you a chance to adjust your plan. If you are falling behind, you need to adjust. You can increase your monthly savings amount, extend your target date, or reduce your target amount. If you are ahead, you may consider raising your goal or distributing the extra money to other goals. Do not cling to a plan that no longer fits you just because you fear making changes.

Life changes, and your goals change with it. Marriage, children, job changes, and moving can all shift your financial priorities. When major changes occur, reassess your goals and adjust your plan accordingly. This does not mean your previous plan was wrong. It simply means your life has changed, and your plan needs to keep up.

Short-term goals and long-term goals are not opposites. You do not need to make an extreme choice between enjoying the present and saving for the future. This is a common misconception. Some people believe that any present consumption steals from future wealth. Others believe that since the future is uncertain, they might as well spend everything now. Both extremes are unhealthy. A healthy financial plan includes both. You save for the future, but you also leave room to enjoy the present. The key is finding the right balance for you. That balance depends on your income, your responsibilities, your values, and your expectations for the future.

Finally, remember that financial goal planning is an ongoing process, not a one-time event. The plan you make today may no longer apply five years from now. This is not failure. This is life. Review regularly, adjust regularly, and stay flexible. The best plan is the one you can stick with, not the one that is mathematically optimal but impossible for you to follow.